Most Real Estate Team Leaders Are Losing Out on Business by Making This Simple Marketing Mistake

Being a team leader can be like being a bird bringing back food to feed a nest full of hungry babies. Without you feeding leads

If you’ve been searching for a house for any amount of time, you’re probably well aware of how important it is to get a mortgage pre-approval before you even start looking at houses, or at least as early on in the process as possible.

But what might come as a surprise to you is that you should also get it updated once in a while — especially considering the current real estate market, because mortgage rates have fluctuated up and down, and it’s often taking buyers longer to find a house to buy.

It might sound like a pain in the neck to have to do it again, but the benefits of spending a few minutes getting your pre-approval updated will make it worth the time spent.

Pre-approvals aren’t good forever. The length of time each lender extends an approval for may vary, but they’re typically good for 60-90 days before they need to be updated or renewed. So, in the least, you’ll want to get it updated whenever your lender’s approval letter expires. But there are other things that can impact your pre-approval during those two to three months which may affect your approval as well.

Here’s a list of things that would indicate it’s a good idea for you to get your pre-approval updated:

Even if none of those apply to you, an up-to-date pre-approval letter will be required by the listings agent whenever you make an offer on a house. So make sure your pre-approval is current at all times to avoid wasting precious time when you find a house you love. Also, submitting one that is outdated could also impact how the listing agent and seller view you, if you don’t look as prepared and thorough as other competing buyers.

The Takeaway:

Even if you’ve already been pre-approved for a mortgage, you might need to get your pre-approval updated on occasion during the process of searching for a home. For starters, they’re only valid for 60-90 days typically. But beyond that, there are a number of factors that could impact your approval within that time frame, so make sure to have your lender update yours if there have been any significant changes in your life, or the market since your first approval was done.

Being a team leader can be like being a bird bringing back food to feed a nest full of hungry babies. Without you feeding leads

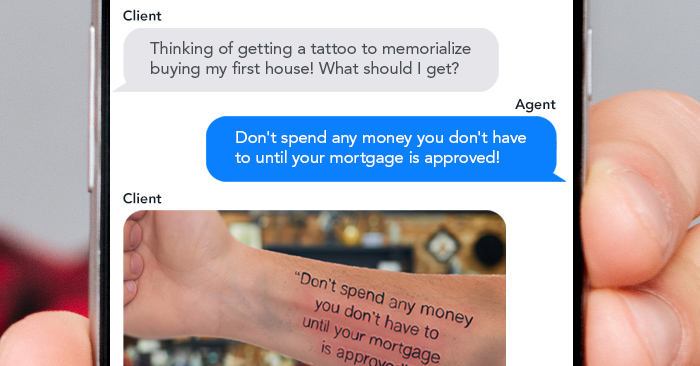

There’s nothing better than working with a client who listens to every piece of advice you give along the way. It makes for a smooth

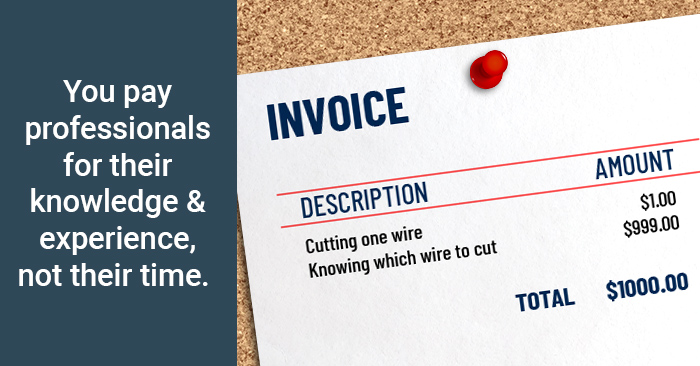

In this spirit of transparency, we admit we’re totally biased when we say “the most clever.” Why’s that? Because we created them. At any rate,

Statistically speaking, the majority of real estate agents don’t make it beyond a couple of years, so don’t feel bad if you’re thinking about giving

There are tons of ways and places to market yourself as a real estate agent, but email marketing has to be one of the best

Depending on your situation, it may not take the full 30 minutes.

This reset password link has expired. Check the latest email sent to you.