One Resolution You Can Easily Stick With To Improve Your Real Estate Business

Raise your hand if you’ve at least mentally made a resolution to sell more houses in the coming year. Every year is a clean slate

By Anita Clark

Let’s face it, you need a strong stomach, a large dose of hang-in-there-and-hold-on-tightly, as well as an ounce or two of patience stored away to make it through a real estate transaction these days. Even “easy” deals can and often do get hung up over minor details. With all the pitfalls ready to snare prospective buyers before they take the keys and begin moving into their love nest, the last thing these consumers need to do is get in their own way!

So, long before you take possession of that cute craftsman, jump for joy at the views from your new condo, or strip down and run around your new private acreage, you need to do everything in your power to avoid these 10 real estate loan killers.

Although it is tempting to sign up for all those snail mail credit card applications, show some restraint, at least until after you close on the home. Getting approved for more credit can actually lower your credit score and give creditors pause about your ability to repay any new debt. The lenders I know are all great peeps, but they universally do not want to suddenly see credit surprises, so do your utmost to avoid the temptation to acquire more credit card bling.

Figuratively, just keep your extra cash under the mattress until you are a new homeowner. When you pay off debt it updates your credit score date of last activity. Generally, while paying off debt early can be a smart move, during the home loan process is not the ideal time to have that revelation, as it can have a negative impact on your credit score. Sleep on the funds and pay off those nagging debts after you have the house keys in hand, not before. If you must indulge, make an extra payment across all your balances at the same time.

The new thingy, bright and shiny, must have, want so badly can nearly taste it, and fill-in-the-blank item can wait! It.Can.Wait. There is no quicker way to sabotage your home loan than to run up your credit cards while waiting for your loan to get through all the wickets. Your credit score will drop quickly and you may find that incredibly reasonable interest rate is no longer available to you, or worse yet, you no longer qualify for the home loan. A good rule of thumb is to ensure your card balances remain below 30% of their available limit.

You could get penalized by moving around your balances and maxing out one (or more) card(s). Again, either wait until you own the property or complete the debt consolidate long before you decide to buy a home. If your lender gives you the green light, go for it, otherwise your best move is to make no move at all.

It can be, especially if you have fully documented where the money came from. Undocumented funds might as well be fool’s gold as your lender will ignore this unsubstantiated cash. The cash may be legit but it cannot be used to verify your income or as a down payment without a paper trail.

This is not a Dr. Phil moment! It is a prudent move to avoid closing credit card accounts while getting a home loan. Your debt ratio will go up, your credit history will be affected, and your lender, agent, significant other, etc. will not be happy with the outcome. Check with your lender before making this move, but the exception is closing old accounts showing an available balance if you believe they are already negatively affecting your credit score.

Wait, what? The less you do to affect your credit the better. Period. That means tasks like creating new accounts, large fund transfers, changing your name, and being a loan cosigner need to wait until after you sign the closing documents.

If your lender tries to contact you and needs you to send them something or call them back, you need to follow their instructions. You need them more than they need you so do everything in your power to be proactive when requests are made.

Please continue making regular payments on all your debt! Do not skip ANY payments. If you do miss a payment let your lender know as quickly as possible so they can determine if/how your loan application has been affected by your faux pas.

Trying to hide credit issues will catch up with you. So will incorrectly reporting income, debt, and your work history. Your lender will find out anyway so it is best to be brutally honest from the beginning. You may be surprised by their willingness to help you, so help yourself by being as transparent as possible.

These are just a few of the ways consumers can get in their own way and sabotage their loan before the ink is dry. If in doubt about the process or approach you need to take, talk with a qualified mortgage professional. Getting and keeping a loan puts you on the path towards home ownership!

Raise your hand if you’ve at least mentally made a resolution to sell more houses in the coming year. Every year is a clean slate

Unless you’re in the process of buying, selling, or refinancing a house, real estate appraisals aren’t something most people think about all that often. So

Having a wedding and buying a house: two of the biggest moments, with two of the biggest price tags in adult life. But lately, it

In this spirit of transparency, we admit we’re totally biased when we say “the most clever.” Why’s that? Because we created them. At any rate,

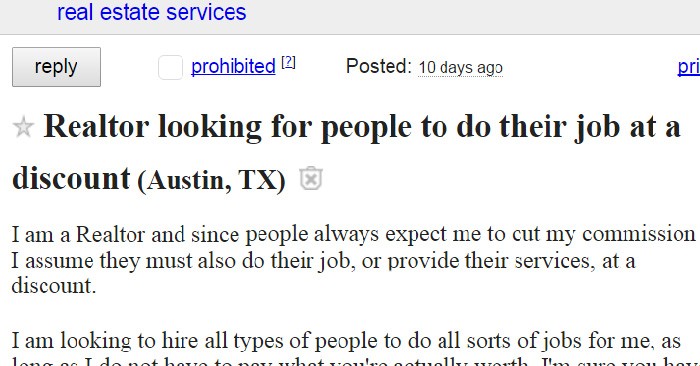

Not everybody who posts to Craigslist is selling or seeking something; some use the platform to make a point. Such is the case with the

Depending on your situation, it may not take the full 30 minutes.

This reset password link has expired. Check the latest email sent to you.